Can Nigerian Businesses Accept Crypto Legally? The 2025-2026 Rules

Imagine a customer in Lagos offering to pay for your goods with Bitcoin. It sounds like the future of commerce, right? But if you are a business owner in Nigeria, that transaction is legally complicated. For years, the rules were murky. Then came a massive shift in 2025. Today, the short answer is: Nigerian businesses cannot accept cryptocurrency as direct legal tender, but they can process these payments if they follow strict new regulations.

The landscape changed dramatically with the passage of the Investments and Securities Act (ISA) 2025. Signed into law by President Bola Ahmed Tinubu on March 29, 2025, this legislation recognized digital assets as securities under the watchful eye of the Securities and Exchange Commission (SEC). This was a huge pivot from the old days when banks were banned from servicing crypto exchanges entirely. However, while trading and investing are now clear-cut legal activities, using crypto as everyday money for buying bread or electronics remains prohibited.

The Core Legal Distinction: Investment vs. Payment

To understand why you can’t just put up a QR code for Bitcoin at your checkout counter, you need to grasp the distinction between an asset and currency. Under the Central Bank of Nigeria Act 2007, only the Naira is legal tender. The ISA 2025 did not change this. Instead, it classified cryptocurrencies like Bitcoin and Ethereum as investment instruments.

This means the government treats crypto similarly to stocks or bonds, not like cash. You can buy them, hold them, and sell them for profit. But you cannot use them to settle debts or pay for daily services directly. The SEC’s official guidance released on April 15, 2025, made this explicit: "Digital assets are recognized as securities and investment instruments, not as currency substitutes for everyday commercial transactions."

So, if a customer wants to pay you in USDT, you technically cannot accept it as final payment. You must convert it to Naira immediately through authorized channels. This creates a specific workflow for merchants that differs significantly from countries like South Africa, where crypto acceptance is more permissive under their Financial Sector Regulation Act.

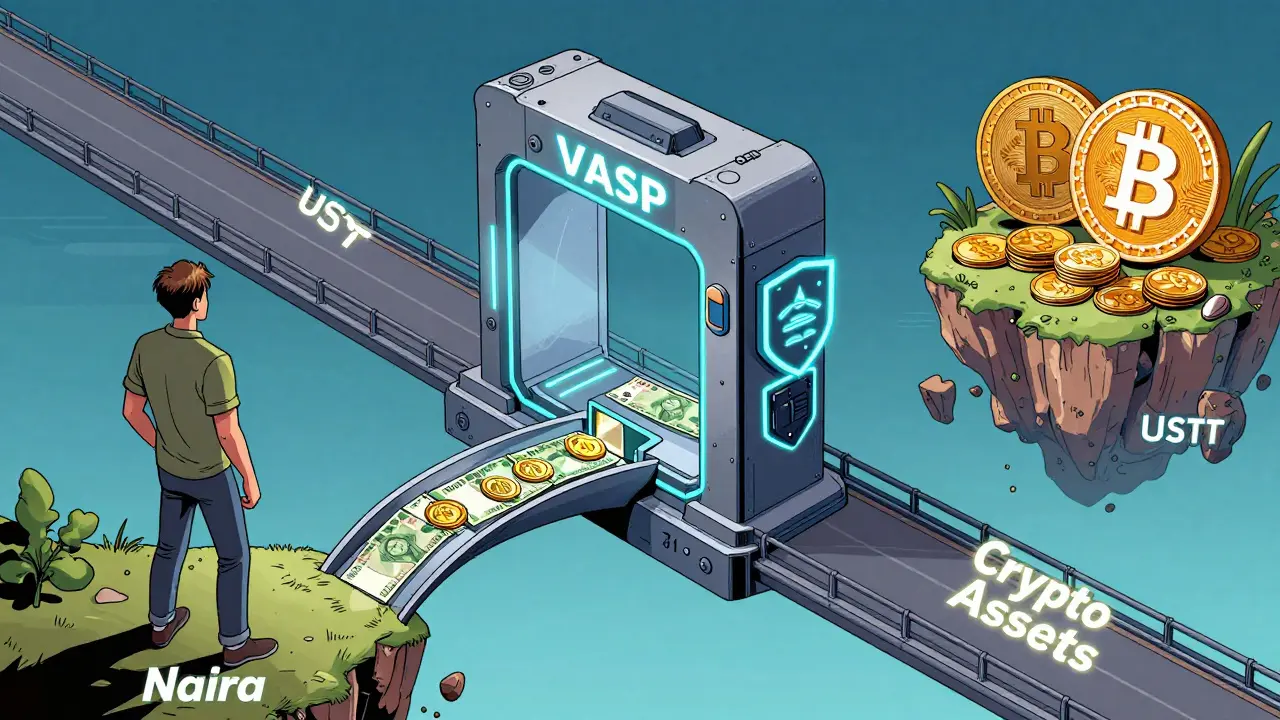

Who Can Actually Process Crypto Payments?

If direct acceptance is off the table, how do some businesses still handle crypto? They don't do it themselves. They partner with licensed intermediaries. The ISA 2025 created three specific categories of entities allowed to touch crypto: Virtual Asset Service Providers (VASPs), Digital Asset Operators (DOPs), and Digital Asset Exchanges (DAEs).

For a regular business-say, an e-commerce store or a consulting firm-you cannot simply decide to become a VASP overnight. The barriers to entry are high. To get licensed by the SEC, a company needs:

- Minimum Capital: At least ₦500 million (roughly $350,000 USD as of late 2025).

- Technical Infrastructure: Systems capable of monitoring transactions 24/7 and handling over 1,000 transactions per second.

- Cybersecurity Standards: Compliance with ISO/IEC 27001 standards is mandatory.

- AML/CFT Protocols: Strict Anti-Money Laundering and Combating Financing of Terrorism procedures, including real-time reporting to the Nigerian Financial Intelligence Unit (NFIU).

As of August 2025, only 47 entities had secured VASP status. These include major players like Quidax, Bybit Nigeria, and Binance Nigeria. If you are not one of these licensed giants, you cannot legally custody or exchange crypto for your customers directly.

| Business Type | Legal Status | Capital Requirement | Primary Function |

|---|---|---|---|

| Regular Merchant | Cannot accept directly | N/A | Must use licensed VASP for conversion |

| VASP (Licensed) | Fully Legal | ₦500 Million+ | Custody, Exchange, Transfer Services |

| P2P Trader | Legal for individuals | None | Personal investment/remittance only |

The Practical Path: How Merchants Operate Today

Since most small and medium-sized enterprises (SMEs) cannot afford the ₦500 million capital requirement, how do they survive? They integrate via APIs provided by the licensed VASPs. Here is how the typical workflow looks for a compliant merchant in 2026:

- Integration: The merchant signs up with a licensed platform like Quidax or Bybit Nigeria.

- Customer Payment: A customer pays in crypto (e.g., Bitcoin or USDT) via the merchant’s checkout page powered by the VASP.

- Instant Conversion: The VASP automatically converts the crypto into Naira.

- Settlement: The Naira is deposited into the merchant’s bank account.

The merchant never actually holds the crypto. This satisfies the regulatory requirement that crypto is an investment vehicle, not a payment method. However, this convenience comes at a cost. Fees typically range from 1.5% to 3.5%, plus potential compliance overheads. According to a survey by Breet.io in July 2025, 78% of merchants who tried accepting crypto before the ISA 2025 stopped after the new rules because the fees and complexity ate into their margins.

One vendor on Jumia complained on social media in September 2025 about having to turn away international customers who wanted to pay in USDT directly, citing the "unnecessary steps and fees" required to route through approved channels. This highlights the friction in the current system.

Risks of Non-Compliance

You might be tempted to bypass the VASP model and accept crypto directly into a personal wallet. Do not do this. The risks are severe. Before the ISA 2025, many businesses operated in a gray area. Now, the SEC has enforcement powers.

In January 2025, a small e-commerce store owner reported receiving a warning letter from the SEC after attempting to accept Bitcoin directly. He was forced to shut down that payment option immediately. Operating without a license violates the SEC’s authorization guidelines. Furthermore, banks are strictly instructed to service only licensed entities. If your bank detects unusual crypto-related flows linked to an unlicensed business account, they may freeze your funds or close your account under the CBN’s circulars.

The goal of these strict rules is investor protection. The SEC reported a 63% reduction in crypto-related scams in the second quarter of 2025 compared to the previous year. By forcing transactions through regulated VASPs, the government aims to prevent fraud and money laundering. While this hurts merchant flexibility, it stabilizes the broader financial ecosystem.

Regional Context: How Nigeria Compares

It helps to look at neighbors to see where Nigeria stands. South Africa allows businesses to accept crypto more freely under its Financial Sector Regulation Act. Kenya, on the other hand, maintains a complete prohibition on crypto as payment for goods. Ghana sits somewhere in the middle, allowing limited acceptance through a regulatory sandbox managed by the Bank of Ghana.

Nigeria’s approach is unique because it classifies crypto as securities. An African Fintech Network analysis from June 2025 scored Nigeria’s framework 7.2 out of 10 for investor protection but only 4.8 out of 10 for merchant adoption friendliness. The report noted that treating crypto as a security creates "unnecessary complexity for businesses seeking to accept crypto as payment."

This classification protects investors from volatile losses and fraudulent schemes but stifles the everyday utility of blockchain technology. Dr. Ngozi Okonjo-Iweala, former Finance Minister, criticized this stance in May 2025, arguing it stifles innovation that could help the 36% of Nigerians who remain unbanked. Conversely, CBN Governor Dr. Olayemi Cardoso defended the approach, prioritizing financial stability over convenience.

What Comes Next? Future Outlook for 2026 and Beyond

The current system is stable but rigid. Recognizing the pushback from the merchant community, the SEC announced a six-month review of the merchant acceptance framework in September 2025. Director General Emomotimi Agama acknowledged the need to balance innovation with stability.

Proposed amendments under consideration include creating a new category called "Digital Payment Vehicle." This would have lower capital requirements-potentially dropping from ₦500 million to ₦50 million-and streamlined compliance. If passed, this could open the door for smaller fintechs and merchants to participate more directly.

Additionally, the Central Bank of Nigeria launched the commercial phase of the eNaira (its Central Bank Digital Currency) in October 2025. With 1.2 million users in the first week, the eNaira offers a state-backed alternative for digital payments. Analysts at Fitch Ratings project that while Nigeria will maintain its securities classification through 2026, limited merchant pathways may emerge by mid-2027.

For now, the strategy for businesses is clear: partner with a licensed VASP. Do not attempt to build your own exchange or hold crypto assets directly unless you are prepared for millions of dollars in compliance costs. The era of wild west crypto spending in Nigeria is over; the era of regulated, secure, and fee-based integration has begun.

Is it illegal to accept Bitcoin in Nigeria in 2026?

It is not explicitly "illegal" in the sense of a criminal ban, but it is non-compliant if done directly. Businesses cannot accept crypto as legal tender. You must process payments through a SEC-licensed Virtual Asset Service Provider (VASP) that converts the crypto to Naira instantly. Direct acceptance without a license violates the Investments and Securities Act (ISA) 2025.

What is the difference between the ISA 2025 and the old crypto ban?

The old ban (pre-2021) prohibited banks from servicing crypto exchanges, pushing activity underground. The ISA 2025 legalized crypto as a security/investment instrument under SEC regulation. It allows trading and investment but maintains that crypto is not legal tender for everyday purchases.

How much does it cost to get a VASP license in Nigeria?

The minimum capital requirement is ₦500 million (approx. $350,000 USD). Additionally, setup costs for technical infrastructure, cybersecurity, and legal compliance range from ₦85 million to ₦200 million. Total initial investment often exceeds $140,000 USD.

Can I use P2P platforms to accept business payments?

Peer-to-Peer (P2P) platforms are primarily designed for individual investment and remittances. Using P2P for business volume can trigger anti-money laundering (AML) flags and violate terms of service. Businesses should use integrated API solutions from licensed VASPs like Quidax or Bybit Nigeria for compliant, automated conversions.

Will the rules change soon to allow easier merchant adoption?

The SEC is reviewing the framework as of late 2025. Proposals include a "Digital Payment Vehicle" category with lower capital requirements (₦50 million). However, analysts expect significant changes no earlier than Q2 2027. For now, the current VASP partnership model is the only safe route.